Revenue loss in subscription apps usually happens not where teams expect it.

Most optimization efforts focus on visible funnel stages such as acquisition and paywall conversion. Yet a meaningful share of revenue loss happens at the level of the payment infrastructure.

Payment failures, card declines, weak retry logic, and regional processing issues may seem minor on their own, but as an app grows, they can compound into significant revenue loss.

In this article, we look at the risks that weak payment setups create as subscription apps scale, where revenue typically leaks, and how to optimise payment infrastructure for scale.

Subscription payments are more complex than they seem

Subscription payments look simple on the surface. But behind every charge there is a set of processes.

From the outside, payments look like a single checkout button. In reality, they are a layered system of billing logic, payment processing, fraud controls, retries, and subscription management working together.

First, the recurring billing logic. A payment does not just need to be processed once. The system must repeat it correctly every billing cycle while accounting for trial periods, upgrades, pauses, cancellations, and plan changes.

Next comes subscription lifecycle management. A subscription moves through multiple states, from trial and active to past-due, paused, or canceled. The billing system must track these states and keep them synced with product access.

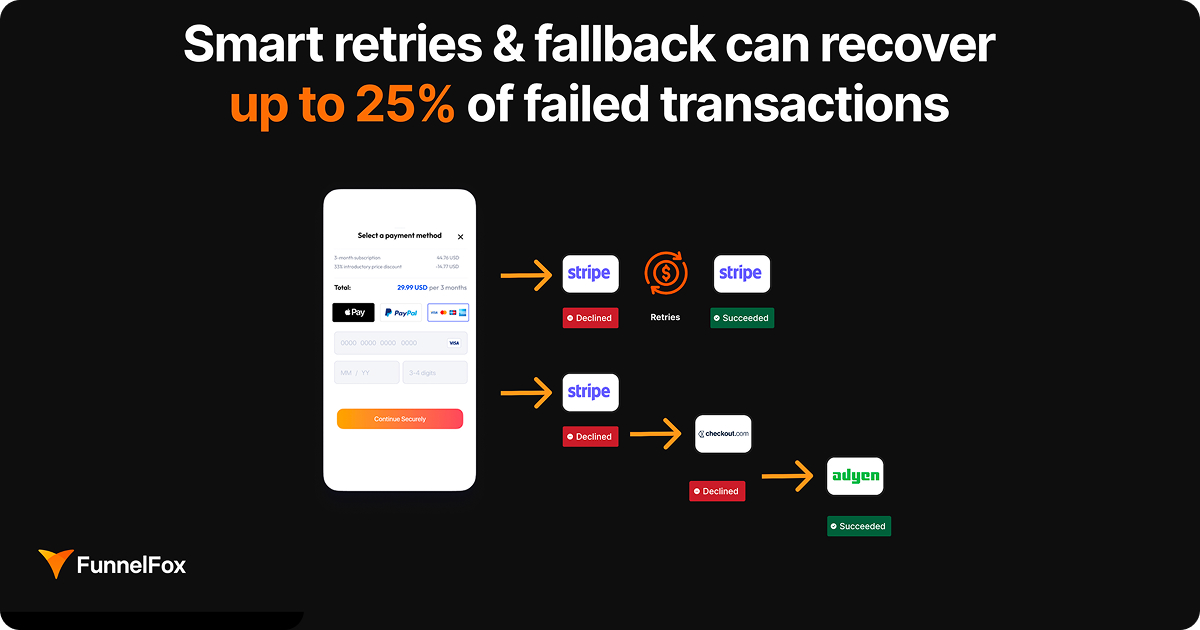

Then there are failed payments and retry logic. Cards expire, banks decline transactions, and users sometimes simply lack available funds. Without structured retry policies and recovery mechanisms, a share of revenue is inevitably lost.

Refunds and disputes require working with banks and payment providers and add another operational layer.

On top of this sit fraud prevention systems that protect the product from stolen card testing, trial abuse, and similar patterns.

And finally, taxes and compliance. Subscriptions are sold globally, so the payment system must account for VAT, regional payment regulations, and data security requirements.

When everything depends on a single payment provider, the system becomes tightly coupled to that provider’s performance and policies.

The risk of relying on a single payment provider

At an early stage, connecting a single PSP is a reasonable choice, but as the business grows, this architecture creates risks.

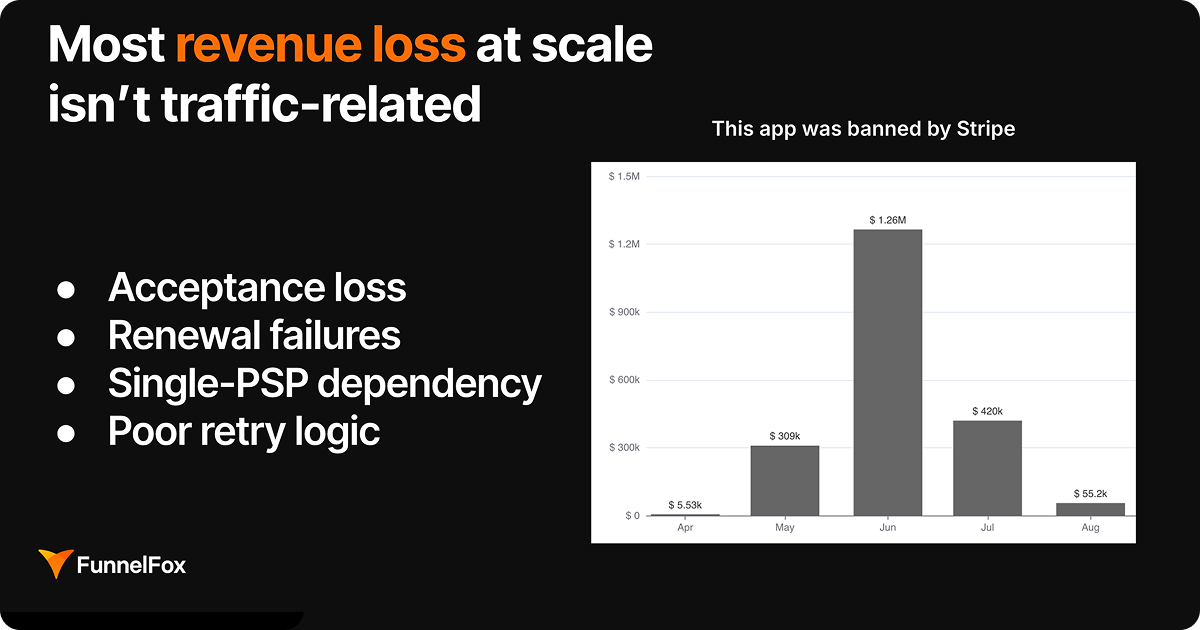

If the entire payment flow runs through one provider, it becomes a single point of failure for revenue.

We see the same pattern over and over: teams build strong funnels, traffic scales up, and then revenue suddenly drops. Acceptance rates go down, renewals fail, or the PSP freezes the account.

Any restrictions, policy changes, or technical issues on the provider’s side immediately affect payments. This creates several risk scenarios.

1. Account freezes or bans

A payment service provider (PSP) may freeze an account due to suspected fraud, a spike in chargebacks, unusual transaction growth, or an automated risk review. This happens regularly, especially with fast-growing products, and if there is no alternative channel, subscription payment processing stops.

If one PSP handles both your payments and your subscription logic, getting banned means you effectively lose everything at once.

2. Provider-specific limitations

Each PSP operates its own acquiring banks, fraud detection models, supported payment methods, and geographic coverage.

If a product relies on a single provider, it also inherits that provider’s limitations: lower payment acceptance rates in certain regions, fewer payment methods, or weaker performance for specific card types.

In other words, the company has little ability to optimize the payment flow.

3. Lack of redundancy in the payment stack

Systems that the business depends on — like payments — should include fallback mechanisms to handle failures. If the payment stack relies on a single PSP, that redundancy simply does not exist, and even a short outage on the provider’s side can result in lost transactions.

The impact of these factors becomes more significant as payment volume grows. When an application processes a small number of payments, the consequences remain limited. But once a meaningful volume of subscriptions flows through the system, dependence on a single PSP creates a revenue risk and losses.

Where do subscription apps lose revenue in their payment infrastructure?

Subscription apps typically lose revenue due to card declines, weak retry logic, checkout friction, and limited regional payment methods.

One of the main sources of revenue losses is card declines and payment failures

Banks regularly decline transactions for many reasons: risk filters, card limits, payment geography, or temporary restrictions on the bank’s side. In international subscription businesses, this happens constantly.

Each declined transaction is a user who wanted to pay but could not complete the payment.

The second issue is weak retry logic

When a payment fails, the system should attempt to process it again. But the outcome depends heavily on the retry strategy: how many attempts are made, how they are spaced, and under what conditions retries are triggered. If the retry mechanism is basic or missing entirely, temporary failures quickly turn into permanently lost payments.

Even if the first payment succeeds, renewals behave very differently. Banks may approve the initial charge but start declining recurring transactions for reasons like insufficient funds, fraud signals, or cross-border processing.

At the same time, smart retry strategies and fallback routing can recover up to 25% of declined transactions.

Next comes checkout friction

Every additional step in the payment flow lowers the chance of completing the payment. Long forms, missing autofill, extra fields, or complex verification often cause users to leave before finishing checkout.

Another issue is limitations around regional payment methods

Not all payment providers handle transactions equally well across regions, banks, or card types. Sometimes a payment fails not because the user cannot pay, but because the transaction is routed through an acquirer that performs poorly in that market.

If a company can’t route payments flexibly or use multiple processing channels, some legitimate transactions simply don’t go through.

On their own, these problems may seem small, but together they can create meaningful revenue loss, especially as the app scales into new markets.

Global growth creates new payment challenges

When a subscription app expands beyond a single market, the payment infrastructure almost always becomes more complex. What works in one country does not always work in another.

One of the first factors is local payment preferences

In some countries, most users pay with cards. In others, local payment methods, bank transfers, or alternative systems dominate. If a product supports only a limited set of methods, some users just won’t be able to pay in the way they normally do.

The next issue is local currencies

In global sales, prices need to be shown in the user’s local currency, and conversion has to be handled correctly. If users see prices in a foreign currency, it can reduce trust and hurt conversion.

Cross-border processing can hurt payment acceptance rates on its own. A merchant entity in one region charging cards issued in another may face more declines even when the user is perfectly legitimate.

Regulatory requirements vary by region

Different countries have their own rules for payment processing, transaction verification, data storage, and refunds. Ignoring locan requirements can lead to restrictions from banks or payment providers.

Another challenge is regional fraud patterns

Fraud levels and common abuse patterns can vary across markets, so antifraud systems need to adjust to these differences. If they don’t, fraud may increase, or legitimate payments may get blocked by overly aggressive filters.

Finally, global sales require proper tax handling

Just as with regulatory requirements, different geos have their own rules for VAT, sales tax, and other taxes on digital services. Handling this correctly requires automated tax calculation and proper reporting in transactions.

As the app scales, these factors start to interact and can affect revenue. Good news: with the right payment infrastructure, you can minimize their impact.

How to build a resilient payment infrastructure for subscription apps

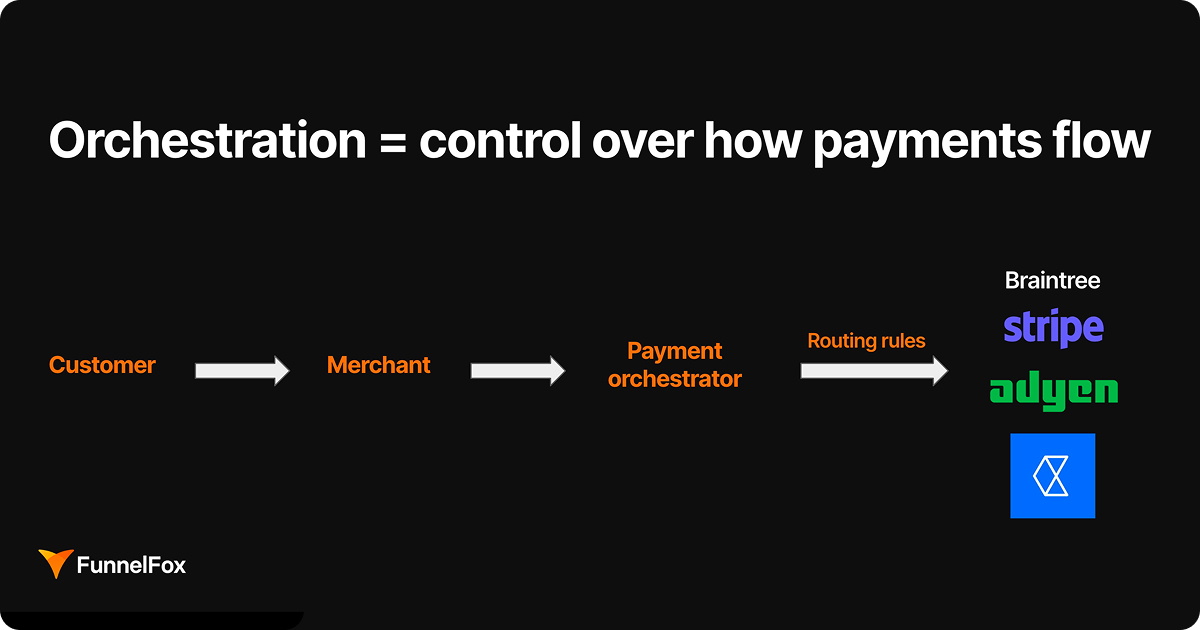

Implement payment orchestration

Orchestration manages how payments flow between different providers. Instead of sending all transactions through a single processor, payment orchestration distributes transactions across multiple systems and optimizes how they are processed.

With orchestration, you get control over the payment flow itself. Instead of sending every transaction through a single provider, you can route payments depending on different parameters: user region, payment method, card type, or the provider’s performance in that market. That gives teams much more flexibility as they scale.

Use multiple payment providers

Using multiple payment providers reduces dependence on a single PSP and lowers the risk of payment failing due to technical issues, account restrictions, or regional processing limitations.

The most important principle is not to rely on a single PSP. If one provider handles both transactions and subscription logic, any ban or freeze becomes a business-wide incident. A multi-provider setup reduces that dependency and gives the business room to keep processing payments even if one channel fails.

Enable payment routing

Payment routing directs transactions through different providers or acquirers depending on factors such as the user’s region, card type, currency, or other parameters. Sending payments through the most suitable processing path improves acceptance rates and reduces the number of declined transactions.

Set up failover systems

Another element of a resilient payment architecture. If the primary payment route fails or a provider is temporarily unavailable, the system automatically sends the transaction through an alternative processor. This reduces the risk of losing payments due to technical failures.

Keep control over checkout and billing flows

When payment logic fully depends on a single provider, optimization options are limited. A more flexible setup allows teams to adjust checkout flows, retry logic, billing cycles, and other parts of the monetization system to match the needs of the product.

As soon as you move beyond a simple one-PSP setup, you need more than payment processing. You need a billing layer that controls how users are charged across upgrades, downgrades, free trials, paid trials, cancellations, migrations, retries, and renewals. That’s what gives teams real control over monetization logic instead of leaving it inside a provider’s default setup.

Once payments are managed this way, the payment stack becomes part of the product’s revenue infrastructure: something that affects conversion, renewals, recovery, and the company’s ability to scale globally without taking unnecessary operational risk.

Why building a payment system in-house is harder than it looks

Once you start scaling, you’ll sooner or later get to the point where you need a more flexible payment architecture. In theory, you can build it in-house. In reality, it quickly turns into a separate infrastructure project. A resilient, flexible payment architecture requires more than just connecting a second PSP.

You’ll need a system that manages billing and subscription logic: upgrades and downgrades, trial periods, plan migrations, cancellations, subscription pauses, and different mobile app monetization scenarios.

Payment routing is also needed to improve acceptance rates and reduce declined payments. Transactions can then be routed through different providers or acquirers depending on the user’s region, currency, or card type.

Then come failover and recovery mechanisms with cascading payment attempts, smart retry intervals, and fallback between providers.

Your payment stack also needs to handle disputes and fraud signals, including early warnings about possible chargebacks and tools for monitoring risk.

All of this adds up to a fairly complex infrastructure. Teams can build it themselves, but it usually takes months of development and ongoing maintenance.

FunnelFox Billing provides web2app payment infrastructure out of the box

FunnelFox Billing provides infrastructure for web payments for subscription apps, allowing teams to manage subscriptions and payment flows without building and maintaining a complex billing system in-house.

The platform includes subscription management for recurring billing, pricing plans, and lifecycle events such as upgrades, downgrades, cancellations, and pauses. It also unifies customer and transaction data across multiple PSPs, so refunds, chargebacks, and other payment operations can be managed from a single system.

FunnelFox Billing also supports payment routing across providers, provider-level and network-level tokenization, and revenue recovery mechanisms such as smart retries and payment cascading. Together, these components help improve payment acceptance rates, maintain billing continuity, and reduce revenue loss from failed payments.

Is your payment infrastructure limiting growth? Book a demo to see how FunnelFox Billing can support it.

Wrap-up on payment infrastructure for subscription apps

Payment infrastructure for subscription apps rarely gets the same attention as acquisition or product features. Yet for subscription apps, it directly affects how much revenue actually reaches the business.

As apps scale across markets and payment volumes grow, small inefficiencies in billing logic, retry strategies, and payment routing start to compound. Without a resilient payment architecture, these issues quietly reduce revenue even when the rest of the funnel performs well.

Designing a flexible payment stack — with orchestration, multiple providers, smart retry logic, and proper subscription management — allows teams to maintain payment continuity as they scale globally.

At that point, payments stop being a hidden operational risk and become part of the product’s growth infrastructure.