TL;DR

- Payment routing determines which payment service provider or acquirer processes a given transaction. Static routing applies a fixed path to every payment. Intelligent routing makes a separate decision per transaction — based on geography, card type, issuer behavior, risk signals, and prior failure history — and adapts when conditions change.

- Failed payments in subscription models drive up to 20% of churn and cost businesses up to 9% of annual revenue. A significant portion of those failures is caused by a suboptimal route. Intelligent routing reduces technical declines upfront and recovers failed payments through route-aware retries.

- To implement an intelligent payment routing system, you need a routing decision engine, a multi-PSP or multi-acquirer setup, a token vault or token portability, retry and fallback logic, and real-time monitoring.

- All of this can be assembled independently, but it requires ongoing engineering. FunnelFox Billing ships smart routing along with retries, tokenization, chargeback prevention, and a unified view of customers and transactions across all providers, so you get full payment infrastructure out of the box.

Intelligent payment routing — also called dynamic payment routing — is an approach where each transaction is routed individually, based on its context and the current performance of available providers. Instead of one fixed path, the system sends each payment through the PSP (payment service provider) or acquirer most likely to approve it.

Intelligent payment routing enables higher payment success rates, fewer failed transactions, and recovered revenue that would otherwise be lost. In subscription models specifically, failed payments drive up to 20% of churn and can cost businesses up to 9% of annual revenue. At that level of revenue impact, payment routing stops being an optimization and becomes a core business variable.

In most setups, it’s one part of a broader payment orchestration system, which manages providers, processing logic, and payment data end to end.

What is intelligent payment routing?

Intelligent payment routing is a system that selects the best route for each transaction based on payment context and the real-time performance of available providers. Its goal is to maximize the chance of a successful charge.

To put it simply, the system decides which PSP or acquirer processes a given payment, taking into account a range of factors: card type, geography, issuer behavior, risk signals, and prior payment history.

What factors affect payment routing decisions?

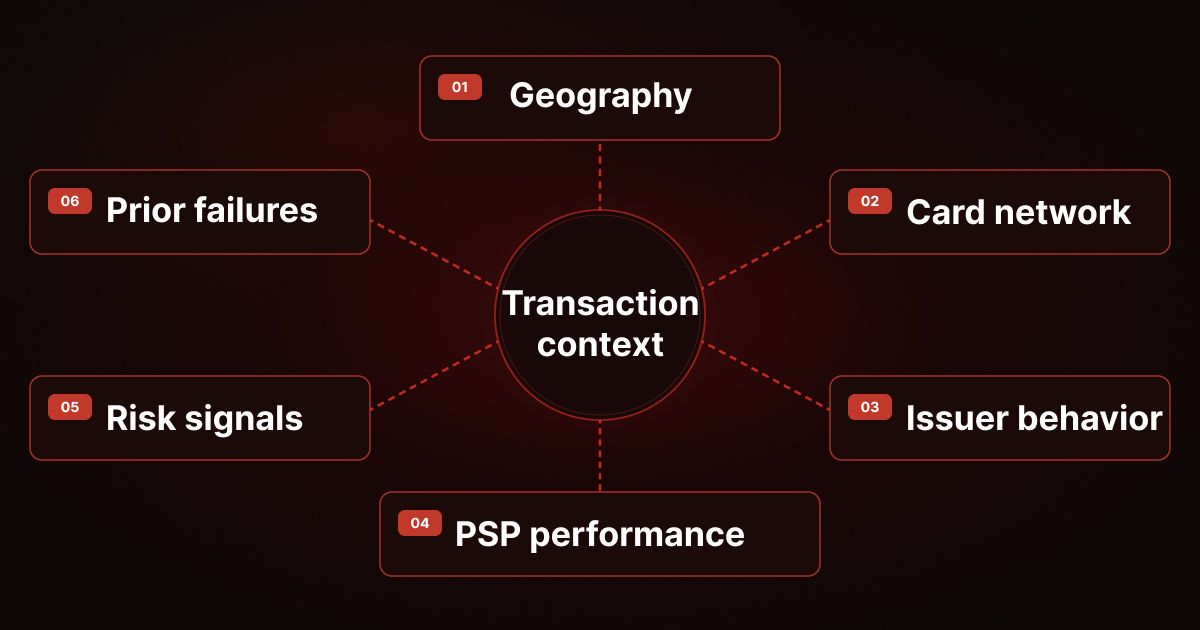

The routing decision is only as good as the signals that inform it. Six factors do most of the work.

1. Geography

A user’s country and their bank’s location directly affect approval rates. The system accounts for country, currency, and regional payment preferences, including which PSPs tend to perform better in specific markets.

2. Card network / card type

Visa, Mastercard, local networks, debit vs. credit: each has its own approval patterns, and some PSPs handle certain card types more reliably than others. Smart payment routing accounts for that difference.

3. Issuer behavior

Not all banks treat transactions the same way, especially recurring ones. Historical data on how specific issuers respond helps the system pick routes with a higher approval rate for that bank.

4. PSP / acquirer performance

Stability, latency, approval rates — these vary across providers, and they change over time. The system routes based on who’s actually performing well right now, not who performed well last month.

5. Fraud and risk signals

Risk scoring shapes not just whether a payment gets processed, but where. Transactions flagged as higher risk may be routed through PSPs with more flexible fraud logic or better 3DS handling.

6. Prior payment failures

This is one of the most valuable signals in the system. If a payment was already declined through one acquirer, the system doesn’t retry the same way — it changes the route, the processing region, or the authentication approach.

These factors don’t operate in isolation. The system weighs them together for each transaction, which is what makes the routing decision intelligent rather than mechanical.

How intelligent payment routing works

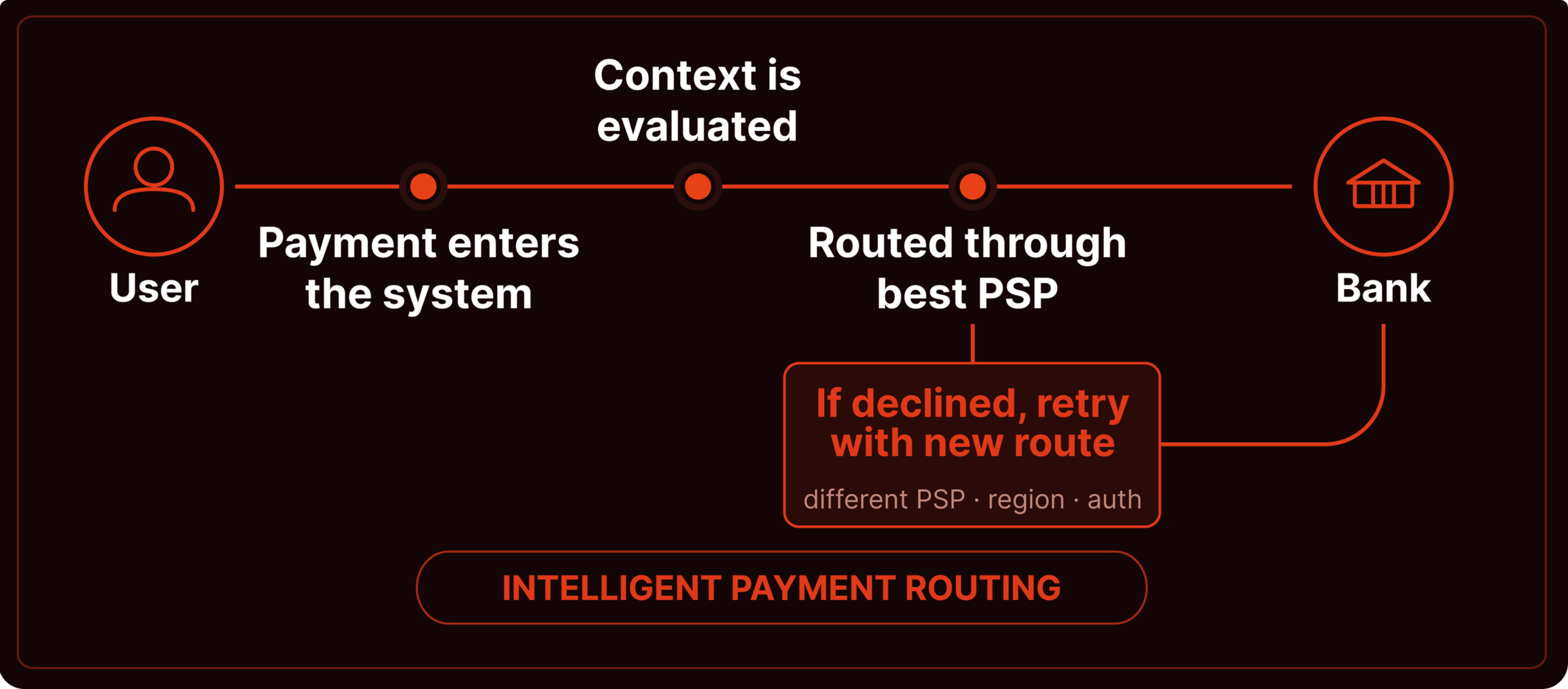

Step 1: A payment enters the system

A payment is initiated, either a first-time purchase or a recurring subscription charge. At this point, the system receives the transaction along with all the context it needs to decide how to process it.

Step 2: The system evaluates the transaction context

The system reads the transaction: geography, currency, card type, issuer, risk signals, and prior failure history. For subscriptions, there’s an additional layer — subscription status, whether this is an initial or recurring charge, and whether there have been previous declines on this account.

Based on that, the system filters out routes that aren’t a good fit for this specific combination of factors. Some paths will underperform for a given issuer or region; others won’t be suitable at all.

Step 3: The payment is routed through the best provider or acquirer

From the remaining options, the system picks one route and sends the payment through a specific PSP or acquirer — not the default one, but the one currently showing the strongest performance for this type of transaction: highest approval rate, fewest declines for this issuer or region, most consistent results.

Step 4: Fallback and retry logic recover failed payments

If the payment is declined, the system doesn’t repeat the same attempt. It changes the approach — different PSP, different acquirer, different processing region, or a different authentication strategy — whatever gives the next attempt the best chance of going through.

This four-step flow runs for every transaction. What changes is the decision at step three — and that decision is only as good as the infrastructure it runs on. Which brings up a question that comes up often: how does intelligent routing differ from static routing, and when does the difference really matter?

Dynamic vs. static payment routing

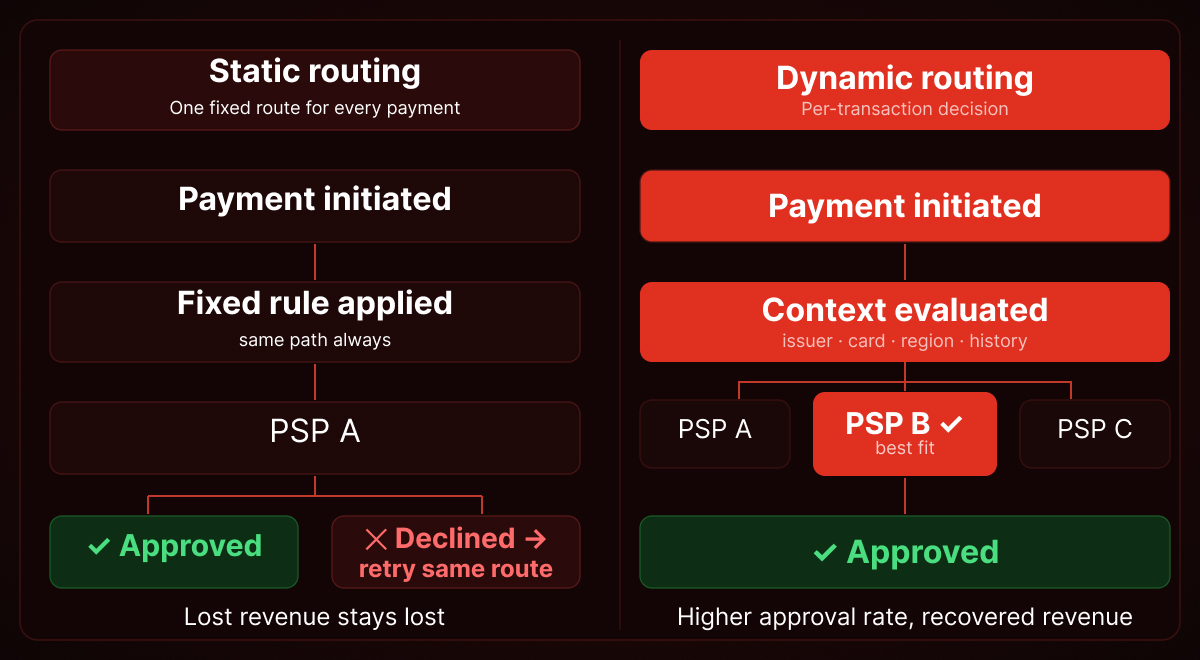

Not all routing works the same way. The difference between static and dynamic comes down to one question: does the system make the same decision every time, or does it adapt?

What is static payment routing?

Static routing means all payments follow a predetermined path. Usually, that’s one primary PSP, or a simple rule set: US traffic goes to provider A, EU traffic goes to provider B. The decision doesn’t change from one transaction to the next, and it doesn’t account for much context.

In subscription models, this hits a ceiling quickly. The same route doesn’t work equally well for different users, issuers, or payment scenarios, and recurring payments make that gap especially visible.

What is dynamic payment routing?

Dynamic routing makes a separate decision for each transaction.

The system evaluates context first — geography, card type, issuer, risk signals, failure history — then selects the provider currently performing best for similar payments. If a payment fails, it can change the route and try again.

The result is a system that adapts to each payment and the conditions around it, rather than applying the same logic regardless of what’s in front of it.

Static vs. dynamic payment routing: key differences

| Aspect | Static routing | Dynamic routing |

|---|---|---|

| Decision level | One predefined route | Per-transaction decision |

| Inputs used | Minimal (e.g., country) | Full context (card, issuer, risk, history) |

| Adaptability | Fixed rules | Adjusts in real time |

| PSP dependency | High (1–2 providers) | Distributed across providers |

| Failure handling | Same retry or no strategy | Route + strategy change on retry |

| Performance optimization | Manual | Continuous, data-driven |

| Scalability | Degrades with complexity | Improves with scale and data |

| Revenue impact | Lost payments stay lost | More approvals, recovered revenue |

Intelligent payment routing vs. payment orchestration

Dynamic routing is a per-transaction decision mechanism. But it doesn’t exist on its own — it runs inside a broader system. That system is payment orchestration, and understanding the difference between the two matters for anyone building serious payment infrastructure.

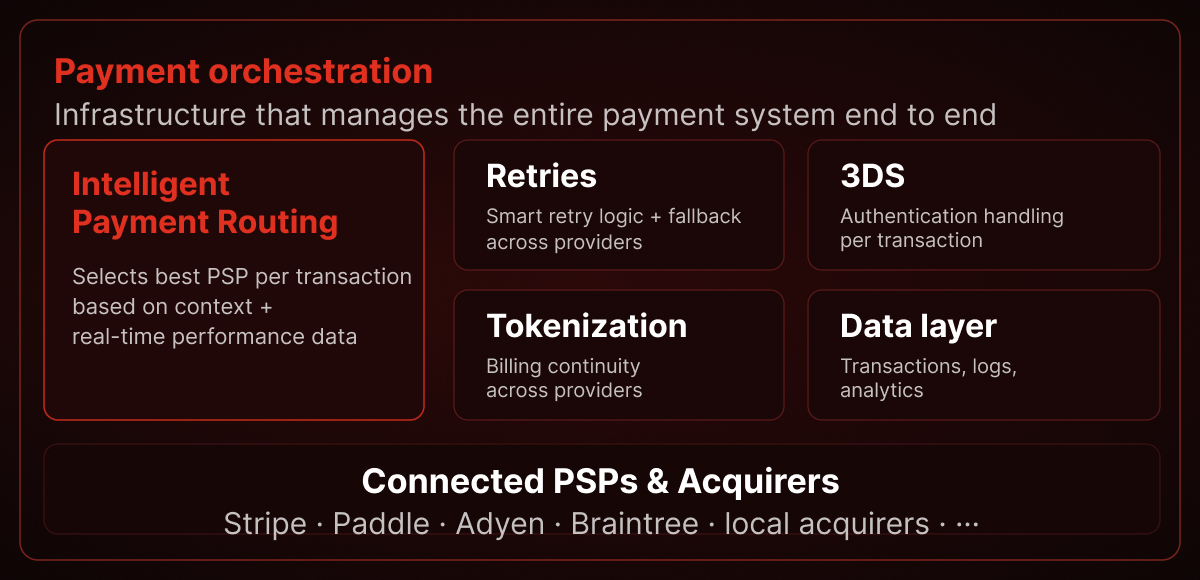

What is payment orchestration?

Payment orchestration is the management system for your entire payment infrastructure. It sits between your product — in the web2app context, your funnel — and all your payment providers, and handles:

- connecting and switching between multiple PSPs

- managing payment logic: routing, retries, 3DS, fallback

- a unified data layer for transactions, logs, and analytics

- simplified integrations — one connection instead of a dozen

Put simply, orchestration is the platform that manages the entire payment process end to end.

How payment orchestration differs from intelligent payment routing

The difference is one of scope.

Intelligent payment routing answers a specific question: which provider should process this payment to maximize the chance of approval? It operates at the transaction level, making decisions based on context and real-time data.

Payment orchestration is the broader system that manages how payments work overall. It connects multiple PSPs, controls processing logic, stores data, and sets the rules under which routing, retries, authentication, and everything else happen.

Routing is a component of orchestration, not an alternative to it. Routing decides where to send a payment. Orchestration defines the system in which that decision gets made and executed.

When businesses need routing vs. orchestration

Routing alone may be enough when:

- you’re working with 1–2 PSPs

- you operate in a single market

- your main goal is improving approval rates

- there’s no complex subscription logic or payment recovery involved

In subscriptions, that’s usually a temporary state.

Orchestration makes sense when:

- you have multiple PSPs or acquirers

- you operate across different regions and currencies

- you run a subscription model with recurring billing, retries, and recovery

- you need to move fast — swap providers, test strategies, and see all payment data in one place

| Aspect | Intelligent payment routing | Payment orchestration |

|---|---|---|

| Scope | One transaction | Entire payment system |

| Purpose | Choose the best route for a payment | Manage how payments are processed overall |

| What it controls | Routing decisions | Providers, routing, retries, 3DS, data |

| Level | Decision-making layer | Infrastructure layer |

| Relationship | Part of orchestration | Includes routing as a component |

Why intelligent payment routing matters

The business case for intelligent routing comes down to one thing: more payments going through, and fewer staying lost. Here’s what that looks like in practice.

Higher payment success rates

Instead of one route for everyone, the system selects the provider that handles this specific transaction type best in this specific context. More payments clear on the first attempt, without any additional action from the user.

Fewer failed payments

Not every decline is the user’s fault. A portion of failures comes from a bad route — a weak combination of issuer and acquirer that doesn’t work well together. When the system accounts for context and avoids those pairings, it reduces the number of technical declines before they happen.

Better payment recovery and less involuntary churn

When failures do occur, the system doesn’t leave them there. Combined with retry logic, intelligent routing changes the route and the processing strategy to reach a successful charge. This directly reduces involuntary churn — cases where the user never intended to cancel, but the payment didn’t go through. That’s where a significant portion of lost revenue gets recovered — smart retries alone can bring back up to 30% of failed payments.

Lower friction for users

Payments go through on the first try more often. Users rarely need to re-enter card details or complete unnecessary authentication steps. From their perspective, checkout just works, and subscriptions stay active without them ever knowing there was a problem to solve.

Better performance across markets and providers

Instead of depending on a single PSP, businesses can use the strengths of different providers and adapt to local market conditions. This matters most in multi-geo setups, where payment performance varies significantly by region. But even within a single market, issuer and provider behavior differ enough that route selection affects outcomes.

That regional variation is worth looking at more closely because the gap between markets is one of the biggest sources of lost approvals that most teams don’t fully account for.

Intelligent payment routing for global payments

Geography affects approval rates more than one can expect. Here’s what drives that and how smart payment routing handles it.

Why payment performance varies by region

Payment approval rates differ by region for specific, structural reasons:

- Issuer behavior. Some banks are aggressive about declining online and recurring payments; others are considerably more permissive.

- Regulatory requirements. Europe’s mandatory 3DS authentication, for example, adds a step that doesn’t exist in every market.

- Local infrastructure. Which acquirers and PSPs perform well in a given country varies significantly.

The result: the same payment, from the same product, can have a high approval rate in one market and a noticeably lower one in another.

How local acquirers and issuer behavior affect routing

Local acquirers tend to be recognized more readily by domestic banks. A payment routed through a local acquirer looks familiar to the issuer — lower risk, less likely to trigger a decline — compared to the same transaction coming through an international provider.

Issuers themselves add another layer of variability:

- some have poor approval rates for recurring payments

- others are sensitive to cross-border transactions

- some require 3DS more frequently than others

Global intelligent payment routing accounts for these differences and selects the acquirer-context combination most likely to clear the bank’s checks.

Why global businesses benefit more from dynamic routing

The more markets you operate in, the more variability you’re dealing with, and the faster a one-size-fits-all route breaks down. In a global setup, you’re managing different regulations, different banks, different user payment preferences, and different provider performance profiles all at once.

Static routing loses payments in this environment because it can’t account for that variation.

Dynamic routing adapts to each country and scenario, uses local acquirers where they have an advantage, and avoids issuer-PSP combinations that underperform in specific markets.

At scale, the difference between static and dynamic routing shows up directly in approval rates and ultimately in revenue.

What you need to implement intelligent payment routing

Dynamic routing requires specific components working together, and missing any one of them limits what the system can do.

A routing decision engine

This is the core of the system. It collects transaction context — geography, card type, issuer, risk signals, failure history — filters out routes that don’t fit, and selects the best one. Without it, there’s no intelligent routing — just a set of providers and no real logic for choosing between them.

Multi-PSP or multi-acquirer setup

If you have one provider, there’s nothing to route between. Intelligent routing requires options — multiple PSPs or acquirers with different geographies, strengths, and approval patterns.

That’s the pool the system distributes traffic across.

Token vault or token portability

Switching between providers requires the ability to move payment credentials with you. Tokens created by one PSP typically don’t work with another.

That means you need either a token vault or token portability support so card data can be reused when the route changes, especially for subscriptions and retries.

Retry and fallback logic

When a payment fails, the system needs to do more than try again. It needs to change something — provider, processing region, authentication approach.

Real-time monitoring and reporting

Without data, routing logic degrades quickly. You need visibility into approval rates by provider, issuer behavior across segments, and where and why declines are happening. The goal isn’t just collecting reports — it’s using that data to update routing logic in real time, or as close to it as possible.

Building all of this takes time and ongoing engineering. For subscription apps running web2app funnels, FunnelFox Billing ships it as a complete stack.

How FunnelFox handles intelligent payment routing

FunnelFox Billing includes smart payment routing as part of its web payments infrastructure built specifically for subscription apps running web2app funnels.

The system routes each transaction across multi PSP based on geography and user segments, with provider-level and network-level tokenization to maintain billing continuity when routes change. Smart retries and payment cascading handle failed payments automatically — no engineering effort required.

The results across FunnelFox customers:

- +11% increase in payment acceptance rate

- +28% recovered revenue after billing issues

- +20% of failed payments recovered through smart retries

Routing is one part of the stack. FunnelFox Billing also handles subscription management, chargeback prevention, and gives you a unified view of customers, transactions, and payment data across all PSPs, all in one place.

Common use cases for intelligent payment routing

Intelligent routing applies across different payment scenarios, but some use cases show its impact more clearly than others.

Subscription renewals and involuntary churn reduction

Routing improves the success rate of recurring charges and reduces declines that have nothing to do with a user’s intent to cancel. Fewer failed renewals means less involuntary churn and higher LTV.

Failed payment recovery flows

When a payment fails, the system changes the route and strategy rather than retrying the same way. That’s how a portion of payments that would otherwise be lost gets recovered.

Cross-border and global payments

Routing accounts for regional differences and directs payments through the most suitable local or international providers — improving approval rates across multi-geo setups.

Multi-PSP resilience and fallback protection

If one provider degrades or goes down, the system automatically shifts traffic to others. Payments keep going through without any visible impact on the user or revenue.

Best practices for payment routing strategy

Having intelligent routing in place is the starting point. Getting consistent results from it requires a few principles that are easy to overlook.

Analyze failed payments before changing routing rules

Not every decline is a routing problem. Before changing anything, identify why payments are failing: insufficient funds, bank restrictions, authentication issues, or provider errors. If the root cause isn’t the route, changing it won’t help.

Use decline-aware retries instead of blind retries

Different decline reasons call for different responses. Some need a different provider, some need 3DS, and some just need a pause before the next attempt. Retries that ignore the decline reason are just extra attempts with no real strategy behind them.

Test routing by market, issuer, and card type

There’s no universally best route. What works well in one country or with one bank can underperform in another segment. The only way to see real differences is to test by market, issuer, card type, and payment type.

Optimize for revenue, not just approvals

A high approval rate itself doesn’t guarantee good economics. You can improve approvals while also increasing fraud, accumulating chargebacks, or eroding margins through provider fees. The right metric to optimize against is net revenue and LTV.

Continuously refine payment routing logic

Issuer behavior, provider performance, and user payment patterns all shift over time, so a route that worked well last month may not be the best option today. Routing logic needs regular review based on fresh data, it’s not something you configure once and leave running.